Copyright © 2022 IFSWF Ltd.

The opinions contained here are those of the authors and do not reflect the views of IFSWF or any of its members.

1. Introduction

To say we live in turbulent times is somewhat of an understatement. No sooner had the pandemic eased its grip on the world, increasingly tense geopolitics and recessionary fears began to dominate the headlines. Monetary stimuli during the pandemic were compounded by food and energy crises that spurred global inflation to levels that appear to be hard to tame. Central bankers in developed markets now need to tread carefully between ensuring financial stability and fighting inflation. While the world has woken up to the need to put climate-change mitigation and adaptation measures in place, more are needed to keep global warming within Paris Agreement targets. Emerging markets, meanwhile, are concurrently battling the energy transition, food security, and sovereign (and maybe corporate) debt crises, and the response of the Bretton Woods institutions has been slow. Consequently, emerging markets’ pre-pandemic development gains have largely been lost. Accomplishing the UN Sustainable Development Goals (SDGs) by 2030 requires annual investments of $4.2 trillion, mostly in sustainable infrastructure, and this huge target appears to be a long way off.

Against this current poly-crisis backdrop, sovereign wealth funds (SWFs) are in a unique position for five reasons.

- Given the size of their assets under management, they can make a meaningful contribution toward achieving the SDGs.

- They are universal asset owners with large stakes in companies across a wide range of sectors and markets

- SWFs are well-placed to drive sustainability across the investment cycle by exercising active and responsible ownership, extending their influence to their investees. The inter-generational nature of SWFs’ investment horizons makes it imperative they assess the materiality of long-term risks, such as climate change, in their portfolios.

- The inter-generational nature of SWFs’ investment horizons makes it imperative they assess the materiality of long-term risks, such as climate change, in their portfolios.

- SWFs are part of the public sector, with different mandates ranging from fiscal revenue stabilisation and intergenerational savings to national economic development, which enables them to have a wide range of impacts across the global economy.

Given these characteristics, SWFs can consider externalities and the need to invest in the broader public good. But they must also invest like private-sector institutions with long investment horizons, securing returns appropriate for the risks taken so that they stay aligned with their organisations’ financial objectives.

Yet, with certain exceptions, SWFs have generally been perceived as isolated institutions, focused on purely financial objectives, and have remained removed from the need to achieve wider development or social objectives, such as delivering the SDGs. For example, in 2019, when asked whether their boards and beneficiaries asked about such issues, only 38% of SWFs said that they did, against around two-thirds of central banks, foundations, and endowments, and just over half of pension funds.

A useful baseline to the analysis in this article is another study performed on the 2000-2020 SWF investment activity and the trends during this period. This previous study, covering a longer period, more transactions, but fewer SWFs, revealed that during the 2000-2020 period, only 16% of the SWFs’ deal count and 7% of their deal value aligned with the SDGs. Still, this study also revealed a noticeable uptick in SDG investing by SWFs from 2018 onwards, particularly in terms of deal values in climate and energy. While the data sets are not directly comparable, the relatively low but growing engagement by SWFs with the SDGs reported in the study culminated in a high point of nearly 100 SDG deals and a total deal value of USD 6.3 billion in 2020, the single year of overlap between the study and this article.

In this article, we would like to examine whether SWFs continue to increase investments aligned with the SDGs. This trend would align with findings from research conducted by IFSWF in 2022, which revealed that SWFs had meaningfully increased their engagement and actions on climate change and were making inroads into looking at social issues.

Most of the information on this topic is derived from surveys. We instead took a “revealed preference” approach, sifting SWF orientation (or lack thereof) towards sustainable investing by analysing their investments between 1 January 2020 and 31 December 2022. We adopted UNEP’s broad definition of “sustainability”, which contains both environmental and economic inclusivity dimensions, and labels SWF deals as sustainable (or SDG-aligned) when executed in the sectors aligned with the IRIS+ taxonomy, a standard reference in the field.

2. Trends

Our sample in the database consisted of 1,092 transactions, of which 310 (28%) were marked as sustainable (SDG) transactions, representing a total of USD 39.3 billion (19%) in deal value. Hence, the SDG transactions only appear to be a relatively minor part of the overall SWF investment activity during the timeframe.

However, when we zoom out to a longer period, we know from another study on SWF investment activity between 2000 and 2020 that the SDG transactions in the 2020-2022 period represent a higher – and growing – percentage of SWF investment activity than in years past. This previous study reported that, overall, during the 2000-2020 period, only 16% of the SWFs’ deal count and 7% of their deal value was aligned with the SDGs. However, the study also revealed a noticeable uptick in SDG investing by SWFs since 2018, especially in terms of deal values in climate and energy.

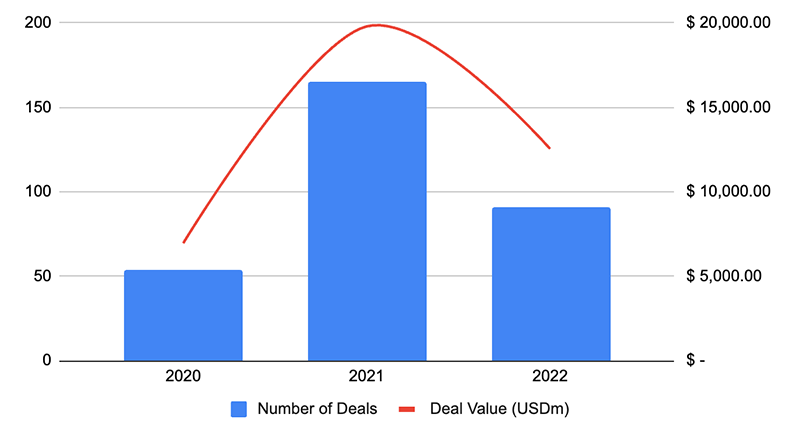

Between 2020 and 2022, we observe a significantly higher SDG deal count materialise in 2021 (165 deals vs 54 deals in 2020) amid higher dealmaking in general (a total of 310 deals in 2021 vs 266 in 2020), to only come down again in 2022 to 91 SDG deals. The overall deal value remained largely flat, but the SDG deal value peaked in 2021 in line with the overall amount invested by SWFs that year, which was the highest annual value on record. When we isolate the SDG deal activity in Figure 1.3, we more clearly observe the spike in SDG deal count and value in 2021. The SDG deal count and deal value increased by nearly three-fold from 2020. Although there was generally more dealmaking in 2021, SDG-aligned deals made up slightly over one third of all deals done, while in 2020, this was only one-fifth. This was, of course, in the middle of the pandemic, and this rapid increase is largely due to the large number of deals done in the healthcare sector.

SWF SDG Investments

Looking at the data from a sectoral perspective, it is obvious that the pandemic catalysed SWF's direct equity investment activity in healthcare. This sector represented 42% of the SDG deal count between 2020 and 2022 (131 SDG deals) and 34% of SDG deal value (USD 12.8 billion). Several SWFs backed the research and development efforts in hot pursuit of a COVID-19 vaccine. For the winners, these high-risk investments are where the public good and financial returns converged.

One of the most notable healthcare investments during the pandemic was by Singapore’s Temasek Holdings, which invested in NASDAQ-listed, Germany-based BioNTech, which partnered with pharmaceutical giant Pfizer to get their COVID-19 vaccine to the market as fast as possible. The vaccine was developed using BioNTech’s innovative, proprietary mRNA technology and leveraged Pfizer’s antigen expertise.

Meanwhile, in June 2021, Singapore’s GIC invested in Medline Industries at an enterprise value of USD 34 billion. The company is the biggest private US manufacturer and distributor of medical supplies like gloves, gowns and examination tables to hospitals and doctor’s practices. The consortium acquiring Medline Industries included private equity firms Blackstone, Carlyle, and Hellman & Friedman.

Likewise, in June 2022, Abu Dhabi’s Mubadala Investment Company invested in Envirotainer. This Swedish company designs, manufactures, and leases active temperature-controlled containers used primarily for airfreighting biopharmaceutical products alongside private equity firm EQT. With a fleet of approximately 6,700 containers globally, the company serves many blue-chip global pharmaceutical and biotech companies. It currently enables the safe delivery of approximately 2 million doses of medicines per day around the globe.

The second-most popular SDG-related sector for sovereign wealth funds between 2020 and 2022 was energy. This sector accounted for 21% of the SDG deal count (65 SDG deals) and 31% of SDG deal value (USD 11.9 billion). Compared to healthcare, SWFs’ investments in energy tend to have larger ticket sizes, as they tend to rely on large infrastructure projects in developed markets with well-understood and proven business and revenue models.

For example, one of the noteworthy transactions in the energy sector was the Abu Dhabi Investment Authority’s acquisition of a 10% interest in Sempra Infrastructure Partners in December 2021. Sempra is a listed NYSE-listed company, one of the largest energy networks in North America, focused on advancing the global energy transition in the markets it serves, including California, Texas, Mexico, and the LNG export market.

Norway’s Government Pension Fund Global (GPFG), the world’s second-largest sovereign wealth fund, completed only three SDG deals during the period. These included a USD 1.63 billion acquisition of a 50% interest in two offshore wind farms, Borssele 1 and 2 in the Netherlands, from Denmark’s Orsted. The wind farm can generate 752 MW of clean energy, sufficient to power a million households annually. This was the SWF’s first investment in unlisted renewable infrastructure and part of its strategy to build a portfolio of wind and solar power generation assets. It must be noted, however, that direct infrastructure represents less than 1% of GPFG’s investments, as the fund typically implements ESG strategies in its listed equity and fixed-income portfolios. These are not evident in the direct investment activity described in this paper.

While this is a relatively small sample, we can make three observations:

- While SWFs are generally thought of as large ships that are hard to turn around, several SWFs stepped up quickly and decisively during the pandemic to help fund the design and scale-up of the manufacturing of the acutely needed vaccines, medical supplies and supply-chain technologies needed to save lives and bring global lockdowns to an end.

- Despite an obvious investment case for renewable energy, given the cost-competitiveness of wind and solar relative to fossil fuels, SWFs have been less enthusiastic about climate change mitigation, resilience, and adaptation investments. However, as SWFs are investors with long investment horizons, these investments have the potential to have complementary return characteristics, particularly as SWFs increasingly understand the financial impact of climate change on their portfolios.

- As the examples in this section suggest, between 2020 and 2022, sovereign wealth funds’ SDG-related investments concentrated on developed countries. For instance, North America accounted for 42% of all SWFs’ SDG-related investments and $15.4 billion, 56.5% of the total, despite developing markets needing far more SDG-aligned investing.

3. Conclusions

In this article, we have attempted to quantitatively document the evolution of SWF sustainable investment during the 2020-2022 period based on the available data on direct equity investments by 77 SWFs. In and of itself, it is hard to draw definitive conclusions from this relatively small and short sample. Of the sample, 28% of the deals worth 19% of the total invested were marked as SDG-related transactions. Hence, the SDG transactions appear to be only a relatively minor part of the overall SWF investment activity during the timeframe.

However, a different reality reveals itself when we zoom out to a longer period. We know from another recent study on SWF investment activity between 2000 and 2020 that SDG transactions now represent a higher – and growing – percentage of SWF investment activity than in years past. We should note that the comparability of the two studies is not entirely straightforward, but the longer-term trends point to a trend of SWFs investing more in sustainable investment sectors, which supports the trends revealed by recent survey-based research.

While SWF’s overall engagement in SDGs may still be somewhat limited, sovereign wealth funds are increasingly engaged. This research revealed a noticeable trend that the COVID-19 pandemic catalysed greater sovereign wealth fund interest in the healthcare sector. Several SWFs have backed the R&D efforts of select pharmaceutical and medical firms in hot pursuit of a COVID-19 vaccine, which helped reduce infection rates and bring pandemic measures to an end.

Despite being asset owners with intergenerational investment horizons and formidable financial firepower, SWFs are not the answer to the world’s poly-crises of the energy transition, food security, and emerging-market debt. Nevertheless, they can play a role, and their SDG alignment is evolving, and meaningful progress has recently been achieved. As overarching themes such as sustainability, climate change mitigation and adaptation, SDGs and SDG investing become more important for asset owners, one might also expect SWFs to align their investment strategies with the SDGs. They might move from relative isolation from external pressures to a universal recognition that they should be part of the solution to our planet’s most pressing problems. Granted, it is easier to evolve when desirable developmental returns pair with compelling financial returns that compensate for the risks taken. The litmus test may well determine SWFs’ future levels of investment activity in critical sectors such as regenerative agriculture (in response to food insecurity), water (in response to growing global scarcity), and climate change mitigation and adaptation (in response to the acute climate crisis unfolding everywhere).

Footnotes

- This is an extract of an article published by the same authors as a result of the research partnership between the Transition Investment Lab and the International Forum for Sovereign Wealth Funds (IFSWF).